Companies Can Deal With the Nonconvertibility Problem of Currencies by Engaging in

U.s.a. lawmakers discussing the Currency Harmonization Initiative Through Neutralizing Action (People's republic of china) Act of 2005

Currency intervention, likewise known as foreign exchange market intervention or currency manipulation, is a budgetary policy operation. It occurs when a regime or key bank buys or sells foreign currency in exchange for its own domestic currency, more often than not with the intention of influencing the exchange charge per unit and merchandise policy.

Policymakers may intervene in strange substitution markets in order to advance a diverseness of economic objectives: controlling inflation, maintaining competitiveness, or maintaining financial stability. The precise objectives are likely to depend on the stage of a country'southward development, the caste of financial market place development and international integration, and the state's overall vulnerability to shocks, among other factors.[one]

The well-nigh complete type of currency intervention is the imposition of a fixed exchange rate with respect to some other currency or to a weighted average of another currencies.

Purposes [edit]

In that location are many reasons a country's monetary and/or fiscal authorization may desire to intervene in the foreign exchange market place. Central banks generally agree that the primary objective of strange commutation market intervention is to manage the volatility and/or influence the level of the exchange rate. Governments prefer to stabilize the exchange rate because excessive brusk-term volatility erodes market place confidence and affects both the financial market and the existent appurtenances market.

When there is inordinate instability, exchange rate uncertainty generates actress costs and reduces profits for firms. Equally a outcome, investors are unwilling to make investment in foreign fiscal assets. Firms are reluctant to engage in international trade. Moreover, the exchange charge per unit fluctuation would spill over into the other fiscal markets. If the exchange rate volatility increases the take chances of holding domestic assets, then prices of these assets would also get more volatile. The increased volatility of fiscal markets would threaten the stability of the financial organisation and brand monetary policy goals more difficult to achieve. Therefore, authorities deport currency intervention.

In addition, when economic conditions change or when the market place misinterprets economical signals, authorities use strange commutation intervention to correct exchange rates, in order to avoid overshooting of either direction. Anna Schwartz contended that the central bank tin can cause the sudden collapse of speculative excess, and that it tin can limit growth by constricting the money supply.[2]

Today, forex market intervention is largely used by the central banks of developing countries, and less then past developed countries. There are a few reasons most adult countries no longer actively intervene:

- Research and experience suggest that the instrument is only effective (at least beyond the very short term) if seen as foreshadowing interest rate or other policy adjustments. Without a durable and independent impact on the nominal substitution rate, intervention is seen as having no lasting ability to influence the existent exchange rate and thus competitive conditions for the tradable sector.

- Large-scale intervention tin can undermine the stance of monetary policy.

Developing countries, on the other hand, do sometimes intervene, presumably because they believe the instrument to exist an effective tool in the circumstances and for the situations they confront. Objectives include: to control aggrandizement, to reach external residuum or heighten competitiveness to boost growth, or to forestall currency crises, such as big depreciation/appreciation swings.[3]

In a Bank for International Settlements (BIS) paper published in 2015, the authors draw the common reasons central banks intervene. Based on a BIS survey, in foreign substitution markets "emerging market cardinal banks" use the strategy of "leaning confronting the wind" "to limit exchange rate volatility and shine the tendency path of the exchange rate".[4] : 5, 6 In their 2005 meeting on foreign commutation market intervention, primal bank governors had noted that, "Many central banks would argue that their main aim is to limit substitution rate volatility rather than to run into a specific target for the level of the exchange rate". Other reasons cited (that do not target the commutation rate) were to "slow the charge per unit of alter of the exchange rate", "dampen commutation rate volatility", "supply liquidity to the forex marketplace", or "influence the level of strange reserves".[5] : 1

Historical context [edit]

In the Cold State of war-era United States, under the Bretton Woods system of fixed commutation rates, intervention was used to help maintain the exchange charge per unit inside prescribed margins and was considered to be essential to a central bank'south toolkit. The dissolution of the Bretton Woods system betwixt 1968 and 1973 was largely due to President Richard Nixon's "temporary" suspension of the dollar's convertibility to gilded in 1971, afterward the dollar struggled throughout the tardily 1960s in calorie-free of big increases in the price of gold. An effort to revive the fixed exchange rates failed, and by March 1973 the major currencies began to float against each other. Since the end of the traditional Bretton Woods arrangement, International monetary fund members accept been free to choose any form of exchange arrangement they wish (except pegging their currency to gold), such equally: allowing the currency to float freely, pegging information technology to another currency or a basket of currencies, adopting the currency of another country, participating in a currency bloc, or forming part of a budgetary union. The finish of the traditional Bretton Forest organisation in the early on 1970s led to widespread merely non universal currency management.[six]

From 2008 through 2013, central banks in emerging marketplace economies (EMEs) had to "re-examine their foreign exchange marketplace intervention strategies" because of "huge swings in capital flows to and from EMEs.[7] : 1

Quite unlike their experiences in the early on 2000s, several countries that had at different times resisted appreciation pressures suddenly constitute themselves having to intervene against stiff depreciation pressures. The sharp ascent in the US long-term interest rate from May to Baronial 2022 led to heavy pressures in currency markets. Several EMEs sold large amounts of forex reserves, raised interest rates and – equally important – provided the private sector with insurance against substitution rate risks.

—Yard S MohantyBIC 2013

Direct intervention [edit]

Direct currency intervention is more often than not defined as foreign exchange transactions that are conducted by the monetary authority and aimed at influencing the exchange rate. Depending on whether it changes the monetary base or not, currency intervention tin can exist distinguished between non-sterilized intervention and sterilized intervention, respectively.

Sterilized intervention [edit]

Sterilized intervention is a policy that attempts to influence the substitution rate without changing the monetary base. The procedure is a combination of 2 transactions. First, the central bank conducts a not-sterilized intervention by buying (selling) foreign currency bonds using domestic currency that it issues. So the central bank "sterilizes" the effects on the monetary base by selling (buying) a corresponding quantity of domestic-currency-denominated bonds to soak upwards the initial increase (decrease) of the domestic currency. The internet effect of the ii operations is the aforementioned as a bandy of domestic-currency bonds for foreign-currency bonds with no change in the coin supply.[8] With sterilization, whatever purchase of strange exchange is accompanied by an equal-valued auction of domestic bonds.

For case, desiring to decrease the exchange rate, expressed equally the price of domestic currency, without changing the monetary base, the monetary potency purchases foreign-currency bonds, the same action as in the last section. After this action, in lodge to keep the budgetary base unchanged, the budgetary authority conducts a new transaction, selling an equal amount of domestic-currency bonds, so that the total coin supply is dorsum to the original level.

Non-sterilized intervention [edit]

Non-sterilized intervention is a policy that alters the monetary base. Specifically, government affect the exchange rate through purchasing or selling foreign money or bonds with domestic currency.

For example, aiming at decreasing the commutation rate/cost of the domestic currency, authorities could purchase foreign currency bonds. During this transaction, extra supply of domestic currency volition elevate down domestic currency cost, and extra demand of foreign currency volition push up strange currency cost. As a issue, the exchange rate drops.

Indirect intervention [edit]

Indirect currency intervention is a policy that influences the commutation rate indirectly. Some examples are upper-case letter controls (taxes or restrictions on international transactions in assets), and exchange controls (the restriction of trade in currencies).[ix] Those policies may lead to inefficiencies or reduce market confidence, or in the case of exchange controls may lead to the creation of a black market, merely can be used as an emergency damage control.

Effectiveness [edit]

Imports and exports from Argentina 1992 to 2004

Non-sterilization intervention [edit]

In full general, there is a consensus in the profession that non-sterilized intervention is constructive. Similarly to the monetary policy, nonsterilized intervention influences the exchange rate past inducing changes in the stock of the monetary base of operations, which, in turn, induces changes in broader monetary aggregates, interest rates, market expectations and ultimately the commutation rate.[10] Every bit we take shown in the previous example, the purchase of foreign-currency bonds leads to the increase of home-currency money supply and thus a decrease of the exchange charge per unit.

Sterilization intervention [edit]

On the other mitt, the effectiveness of sterilized intervention is more than controversial and ambiguous. By definition, the sterilized intervention has little or no effect on domestic involvement rates, since the level of the coin supply has remained abiding. However, according to some literature, sterilized intervention can influence the commutation rate through 2 channels: the portfolio balance channel and the expectations or signaling channel.[xi]

- The portfolio balance channel

- In the portfolio balance approach, domestic and foreign bonds are non perfect substitutes. Agents remainder their portfolios among domestic money and bonds, and foreign currency and bonds. Whenever aggregate economical weather condition change, agents adjust their portfolios to a new equilibrium, based on a variety of considerations, i.due east., wealth, tastes, expectation, etc.. Thus, these actions to balance portfolios will influence exchange rates.

- The expectations or signaling channel

- Fifty-fifty if domestic and foreign assets are perfectly substitutable with each other, sterilized intervention is notwithstanding effective. According to the signaling channel theory, agents may view exchange rate intervention as a betoken about the future stance of policy. Then the alter of expectation will affect the current level of the exchange rate.

Modern examples [edit]

According to the Peterson Plant, there are four groups that stand out as frequent currency manipulators: longstanding advanced and adult economies, such as Nihon and Switzerland, newly industrialized economies such equally Singapore, developing Asian economies such every bit China, and oil exporters, such as Russia.[12] Prc's currency intervention and foreign exchange holdings are unprecedented.[13] It is common for countries to manage their exchange rate via central banking company to make their exports inexpensive. That method is beingness used extensively by the emerging markets of Southeast Asia, in item.

The American dollar is generally the primary target for these currency managers. The dollar is the global trading system'due south premier reserve currency, pregnant dollars are freely traded and confidently accepted by international investors.[14] System Open Market Account is a monetary tool of the Federal Reserve system that may intervene to counter hell-raising marketplace conditions.[fifteen] In 2014, a number of big investment banks, including UBS, JPMorgan Chase, Citigroup, HSBC and the Royal Bank of Scotland were fined for currency manipulations.[16]

Swiss franc [edit]

As the financial crisis of 2007–08 hit Switzerland, the Swiss franc appreciated "owing to a flight to safety and to the repayment of Swiss franc liabilities funding carry trades in high yielding currencies." On March 12, 2009, the Swiss National Banking company (SNB) announced that it intended to buy strange exchange to preclude the Swiss franc from further appreciation. Affected by the SNB purchase of euros and US dollars, the Swiss franc weakened from 1.48 against the euro to 1.52 in a single day. At the end of 2009, the currency risk seemed to exist solved; the SNB changed its attitude to preventing substantial appreciation. Unfortunately, the Swiss franc began to appreciate once again. Thus, the SNB stepped in one more fourth dimension and intervened at a charge per unit of more than CHF xxx billion per month. By the end of June 17, 2010, when the SNB announced the finish of its intervention, it had purchased an equivalent of $179 billion of Euros and U.South. dollars, amounting to 33% of Swiss GDP.[17] Furthermore, in September 2011, the SNB influenced the foreign substitution market place once more, and set a minimum exchange rate target of SFr 1.two to the Euro.

On January 15, 2015, the SNB suddenly announced that information technology would no longer hold the Swiss Franc at the fixed commutation charge per unit with the euro it had set up in 2011. The franc soared in response; the euro cruel roughly forty percent in value in relation to the franc, falling as low equally 0.85 francs (from the original 1.two francs).[eighteen]

As investors flocked to the franc during the financial crisis, they dramatically pushed up its value. An expensive franc may have big agin effects on the Swiss economy; the Swiss economic system is heavily reliant on selling things abroad. Exports of goods and services are worth over lxx% of Swiss Gross domestic product. To maintain price stability and lower the franc's value, the SNB created new francs and used them to buy euros. Increasing the supply of francs relative to euros on strange-substitution markets acquired the franc's value to autumn (ensuring the euro was worth 1.2 francs). This policy resulted in the SNB amassing roughly $480 billion-worth of foreign currency, a sum equal to about 70% of Swiss Gdp.

The Economist [ citation needed ] asserts that the SNB dropped the cap for the post-obit reasons: commencement, ascension criticisms amid Swiss citizens regarding the large build-up of foreign reserves. Fears of runaway aggrandizement underlie these criticisms, despite aggrandizement of the franc existence too low, co-ordinate to the SNB. Second, in response to the European Primal Bank'south conclusion to initiate a quantitative easing program to combat euro deflation. The consequent devaluation of the euro would crave the SNB to farther devalue the franc had they decided to maintain the stock-still substitution rate. Third, due to recent euro depreciation in 2014, the franc lost roughly 12% of its value against the USD and ten% against the rupee (exported goods and services to the U.Due south. and India business relationship for roughly 20% Swiss exports).

Following the SNB's announcement, the Swiss stock market sharply declined; due to a stronger franc, Swiss companies would have had a more difficult time selling goods and services to neighboring European citizens.[19]

In June 2016, when the results of the Brexit referendum were announced, the SNB gave a rare confirmation that it had increased foreign currency purchases again, as evidenced by a ascension of commercial deposits to the national bank. Negative interest rates coupled with targeted foreign currency purchases have helped to limit the force of the Swiss Franc in a time when the need for rubber haven currencies is increasing. Such interventions assure the price competitiveness of Swiss products in the European Marriage and global markets.[20]

Japanese yen [edit]

From 1989 to 2003, Nippon was suffering from a long deflationary menstruum. After experiencing economic boom, the Japanese economy slowly declined in the early on 1990s and entered a deflationary spiral in 1998. Within this menstruation, Japanese output was stagnating; the deflation (negative inflation rate) was continuing, and the unemployment charge per unit was increasing. Simultaneously, confidence in the fiscal sector waned, and several banks failed. During the menstruation, the Bank of Japan, having go legally independent in March 1998, aimed at stimulating the economy by catastrophe deflation and stabilizing the fiscal organisation.[21] The "availability and effectiveness of traditional policy instruments was severely constrained as the policy interest charge per unit was already virtually at nothing, and the nominal interest rate could not become negative (the zero bound problem)."[22]

In response of deflationary pressures, the Bank of Japan, in coordination with the Ministry of Finance, launched a reserve targeting program. The BOJ increased the commercial banking concern electric current account balance to ¥35 trillion. After, the MoF used those funds to purchase $320 billion in U.Southward. treasury bonds and bureau debt.[23]

By 2014, critics of Japanese currency intervention asserted that the key depository financial institution of Nippon was artificially and intentionally devaluing the yen. Some state that the 2022 The states-Nippon trade deficit — $261.7 billion — was increased unemployment in the The states.[ citation needed ] Bank of Korea Governor Kim Choong Soo has urged Asian countries to work together to defend themselves against the side-effects of Japanese Prime number Minister Shinzo Abe's reflation campaign. Some take (who?) stated this campaign is in response to Nihon's stagnant economy and potential deflationary spiral.[ citation needed ]

In 2013, Japanese Finance Minister Taro Aso stated Japan planned to use its foreign exchange reserves to purchase bonds issued past the European Stability Machinery and euro-area sovereigns, in order to weaken the yen.[ citation needed ] The U.S. criticized Japan for undertaking unilateral sales of the yen in 2011, later on Group of Seven economies jointly intervened to weaken the currency in the aftermath of the tape convulsion and tsunami that year.[ citation needed ]

By 2013, Nippon held $ane.27 trillion in strange reserves according to finance ministry information.[24]

Qatari riyal [edit]

On August 27, 2019, the Qatar Financial Centre Regulatory Dominance, likewise known as QFCRA, fined the First Abu Dhabi Bank (FAB) for $55 million, over its failure to cooperate in a probe into possible manipulation of the Qatari riyal. The action followed a significant amount of volatility in the substitution rates of the Qatari riyal during the commencement eight months of the Qatar diplomatic crisis.[25]

In Dec 2020, Bloomberg News reviewed a big number of emails, legal filings and documents, along with interviews conducted with the former officials and insiders of Banque Havilland. The observation-based findings showed the extent of services that financier David Rowland and his individual cyberbanking service went, in society to serve one of its customers, the Crown Prince of Abu Dhabi, Mohammed bin Zayed. The findings showed that the ruler used the bank for financial communication every bit well every bit for manipulating the value of the Qatari riyal in a coordinated attack aimed at deleting the state's foreign commutation reserves. One of the five mission statements reviewed by Bloomberg read, "Command the yield curve, decide the future." The argument belonged to a presentation made by 1 of the ex-Banque Havilland analysts that called for the attack in 2017.[26]

Chinese yuan [edit]

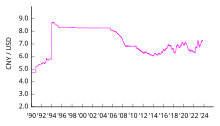

Graph of the price of a United states dollar in Chinese yuan since 1990

In the 1990s and 2000s, there was a marked increment in American imports of Chinese goods. Communist china'due south central bank allegedly devalued yuan by buying large amounts of US dollars with yuan, thus increasing the supply of the yuan in the foreign exchange market place, while increasing the demand for Usa dollars, thus increasing the price of USD.[ citation needed ] According to an article published in KurzyCZ by Vladimir Urbanek, by December 2012, China's foreign exchange reserve held roughly $3.3 trillion, making it the highest strange exchange reserve in the world. Roughly 60% of this reserve was equanimous of US government bonds and debentures.[27]

At that place has been much disagreement on how the United States should answer to Chinese devaluation of the yuan. This is partly due to disagreement over the actual furnishings of the undervalued yuan on capital markets, trade deficits, and the United states domestic economy.[ commendation needed ]

Paul Krugman argued in 2010, that China intentionally devalued its currency to boost its exports to the United states and as a result, widening its trade deficit with the US. Krugman suggested at that time, that the United States should impose tariffs on Chinese goods. Krugman stated:[28]

The more depreciated China's commutation rate — the higher the price of the dollar in yuan — the more dollars Prc earns from exports, and the fewer dollars it spends on imports. (Capital letter flows complicate the story a flake, but don't change it in any fundamental way). By keeping its electric current artificially weak — a higher price of dollars in terms of yuan — Prc generates a dollar surplus; this ways the Chinese government has to purchase up the excess dollars.

Greg Mankiw, on the other paw, asserted in 2010 the U.S. protectionism via tariffs will hurt the U.S. economic system far more than Chinese devaluation. Similarly, others[ who? ] accept stated that the undervalued yuan has actually hurt Communist china more in the long run insofar that the undervalued yuan does not subsidize the Chinese exporter, merely subsidizes the American importer. Thus, importers inside China have been substantially hurt due to the Chinese government's intention to keep to abound exports.[29]

The view that China manipulates its currency for its own benefit in merchandise has been criticized by Cato Plant trade policy studies fellow Daniel Pearson,[30] National Taxpayers Union Policy and Authorities Affairs Manager Clark Packard,[31] entrepreneur and Forbes contributor Louis Woodhill,[32] Henry Kaufman Professor of Financial Institutions at Columbia University Charles W. Calomiris,[33] economist Ed Dolan,[34] William Fifty. Clayton Professor of International Economical Affairs at the Fletcher Schoolhouse, Tufts University Michael W. Klein,[35] Harvard Academy Kennedy School of Authorities Professor Jeffrey Frankel,[36] Bloomberg columnist William Pesek,[37] Quartz reporter Gwynn Guilford,[38] [39] The Wall Street Periodical Digital Network Editor-In-Principal Randall West. Forsyth,[40] United Courier Services,[41] and Prc Learning Curve.[42]

Russian ruble [edit]

On Nov 10, 2014, the Key Banking company of Russian federation decided to fully float the ruble in response to its biggest weekly driblet in 11 years (roughly 6 percent drop in value against USD).[43] In doing so, the central bank abolished the dual-currency trading band within which the ruble had previously traded. The central bank also ended regular interventions that had previously express sudden movements in the currency's value. Before steps to raise interest rates past 150 basis points to ix.5 percent failed to stop the ruble's turn down. The central bank sharply adjusted its macroeconomic forecasts. It stated that Russia's foreign exchange reserves, then the fourth largest in the earth at roughly $480 billion, were expected to subtract to $422 billion by the finish of 2014, $415 billion in 2015, and under $400 billion in 2016, in an effort to prop up the ruble.[44]

On December eleven, the Russian central bank raised the key rate by 100 footing points, from nine.5 per centum to ten.5 percent.[45]

Failing oil prices and economical sanctions imposed by the Westward in response to the Russian annexation of Crimea led to worsening Russian recession. On December 15, 2014, the ruble dropped equally much as nineteen pct, the worst unmarried-day drop for the ruble in xvi years.[46] [47]

The Russian central depository financial institution response was twofold: first, continue using Russia'due south large foreign currency reserve to buy rubles on the forex market in order to maintain its value through bogus need on a larger calibration. The same week of the December 15 drop, the Russian central bank sold an additional $700 meg in foreign currency reserves, in improver to the nigh $30 billion spent over previous months to stave off decline. Russian federation's reserves then sat at $420 billion, down from $510 billion in January 2014.

Second, increase involvement rates dramatically. The cardinal banking concern increased the central interest rate 650 footing points from 10.5 percentage to 17 per centum, the earth's largest increase since 1998, when Russian rates soared by 100 per centum and the government defaulted on its debt. The central bank hoped the higher rates would provide incentives to the forex market to maintain rubles.[48] [49]

From February 12 to xix, 2015, the Russian central bank spent an boosted $six.iv billion in reserves. Russian foreign reserves at this point stood at $368.3 billion, profoundly beneath the central bank's initial forecast for 2015. Since the collapse in global oil prices in June 2014, Russian reserves have fallen past over $100 billion.[50]

As oil prices began to stabilize in Feb–March 2015, the ruble likewise stabilized. The Russian key bank has decreased the key rate from its high of 17 percent to its electric current 15 per centum as of February 2015. Russian foreign reserves currently sit at $360 billion.[51] [52]

In March and Apr 2015, with the stabilization of oil prices, the ruble has made a surge, which Russian authorities accept deemed a "miracle". Over three months, the ruble gained 20 percent against the U.s.a. dollar, and 35 pct confronting the euro. The ruble was the best performing currency of 2022 in the forex market. Despite being far from its pre-recession levels (in January 2014, The states$1 equaled roughly 33 Russian rubles), information technology is currently trading at roughly 52 rubles to US$1 (an increment in value from 80 rubles to US$1 in December 2014).[53]

Current Russian foreign reserves sit at $360 billion. In response to the ruble's surge, the Russian key bank lowered its key interest charge per unit farther to 14 percent in March 2015. The ruble's recent gains have been largely accredited to oil toll stabilization and the calming of conflict in Ukraine.[54] [55]

Come across also [edit]

- Exchange Equalisation Account in the United Kingdom

- Exchange Stabilization Fund in the U.s.a.

- Open market performance

- Quantitative easing

- Forex scandal

References [edit]

- ^ Joseph Due east. Gagnon, "Policy Brief 12-19", Peterson Institute for International Economical, 2012.

- ^ Tim Ferguson (21 June 2012). "Anna Schwartz, Monetary Historian, RIP". Forbes . Retrieved 6 January 2017.

- ^ Bank for International Settlements, BIS Newspaper No. 24, Foreign commutation market intervention in emerging markets: motives, techniques and implications, (2005).

- ^ Chutasripanich, Nuttathum; Yetman, James (2015), "Foreign exchange intervention: strategies and effectiveness" (PDF), Banking concern for International Settlements (BIS), BIS Working Papers, no. 499, p. 34, ISSN 1682-7678

- ^ "Foreign substitution market place intervention in emerging marketplace economies: an overview", Bank for International Settlements (BIS), Foreign commutation market intervention in emerging markets: motives, techniques and implications, no. 24, p. 3, May 2005,

On 2 and three December 2004, the BIS hosted a coming together of Deputy Governors of central banks from major emerging market economies to discuss foreign exchange market intervention.

- ^ Lucio Sarno and Mark P. Taylor, "Official Intervention in the Foreign Exchange Marketplace: Is It Constructive and, If So, How Does It Work?," Periodical of Economic Literature 39.three (2001): 839-68.

- ^ Mohanty, Grand. S. (2013), "Market volatility and strange commutation intervention in EMEs: what has changed?" (PDF), Bank for International Settlements (BIS), BIS Working Papers, no. 73, p. x

- ^ Obstfeld, Maurice (1996). Foundations of International Finance . Boston: Massachusetts Institute of Engineering science. pp. 597–599. ISBN0-262-15047-6.

- ^ Neely, Christopher (November–December 1999). "An Introduction to Majuscule Controls". Federal Reserve Depository financial institution of St. Louis Review: 13–30.

- ^ Tyalor, Marker; Lucio Sarno (September 2001). "Official Intervention in the Foreign Exchange Market: Is It Constructive and, If And then, How Does It Work?" (PDF). Periodical of Economical Literature: 839–868.

- ^ Mussa, Michael (1981). The Role of Official Intervention. VA: George Mason University Press.

- ^ Joseph East. Gagnon, "Policy Cursory: Combating Widespread Currency Manipulation", Peterson Establish for International Economic science, (2012).

- ^ Munson, Peter J. (2013). State of war, Welfare & Democracy: Rethinking America's Quest for the Finish of History. Potomac Books, Inc. p. 117. ISBN978-1612345390 . Retrieved 9 Jan 2017.

- ^ Jared Bernstein, "How to Terminate Currency Manipulation", The New York Times, 2015

- ^ "System Open Market Account". New York Fed. Retrieved 5 January 2017.

- ^ Sovereign Wealth Fund Constitute. "Hands Slapped: v Banks Get Hit with Fines for Currency Manipulation". Archived from the original on 20 March 2016. Retrieved five January 2017.

- ^ Gerlach, Petra; Rober McCauley; Kazuo Ueda (October 2011). "Currency Intervention and the Global Portfolio Balance Effect". Paper.

- ^ "Swiss franc jumps 30 percentage after Swiss National Bank dumps euro ceiling". Reuters. January xv, 2015.

- ^ "Why the Swiss unpegged the franc". The Economist. January eighteen, 2015.

- ^ "Swiss National Bank ramps upward currency intervention after Brexit" . Reuters. July 4, 2016.

- ^ Takatoshi Ito, "Japanese Monetary Policy: 1998-2005 and Beyond," Bank of International Settlements, p.105-107.

- ^ Takatoshi,p.105.

- ^ Richard Duncan, The Dollar Crisis: Causes, Consequences, Cures, (2011).

- ^ Mayumi Otsuma, "Nihon to Buy European Debt with Currency Reserves to Weaken Yen", Bloomberg News, 2013: par. ane-8.

- ^ "QFC fines Abu Dhabi bank over currency manipulation". The Economist . Retrieved 6 September 2019.

- ^ "At Banque Havilland, Abu Dhabi'south Crown Prince Was Known every bit 'The Boss'". Bloomberg . Retrieved 21 December 2020.

- ^ Urbanek, Vladimir (4 March 2013), "China's foreign exchange reserves at the end of 2022 grew to 3.3 trillion, from +700% Fifty.04", KurzyCZ, archived from the original on 18 May 2015, retrieved 5 May 2015

- ^ Krugman, Paul (Feb iv, 2010). "Chinese Rumbles". The New York Times . Retrieved May 16, 2017.

- ^ Jonathan Yard. Finegold Catalan, "A Closer Look at Prc's Currency Manipulation", Ludwig von Mises Institute, (2010).

- ^ "PolitiFact - Trump says Red china gets an advantage from the Trans-Pacific Partnership". Retrieved 2016-08-03 .

- ^ "National Taxpayers Union - Donald Trump Wrong on Trade". www.ntu.org . Retrieved 2016-08-03 .

- ^ "Donald Trump Should Apologize to China, and Plow His Wrath On the Fed | RealClearMarkets". Retrieved 2016-08-03 .

- ^ Calomiris, Charles Due west. "Trump Gets His Facts Incorrect On China". Forbes . Retrieved 2016-08-03 .

- ^ "Economic News, Assay, and Discussion".

- ^ http://www.brookings.edu/research/opinions/2015/05/22-china-and-currency-manipulation-klein

- ^ Frankel, Jeffrey (2015-02-20). "The Non-Problem of Chinese Currency Manipulation". Retrieved 2016-08-03 .

- ^ Pesek, Willie (2015-05-28). "Terminate Calling China a Currency Manipulator". Bloomberg View . Retrieved 2016-08-03 .

- ^ Guilford, Gwynn. "Donald Trump has no thought what he's talking about on Communist china". Retrieved 2016-08-03 .

- ^ "Donald Trump Has No idea What He's Talking Well-nigh on Red china". Retrieved 2016-08-03 .

- ^ Forsyth, Randall W. "Trump Is Wrong on China". Retrieved 2016-08-03 .

- ^ "TRUMP Wrong Well-nigh CHINA'S CURRENCY MOVE". Retrieved 2016-08-03 .

- ^ "Why Donald Trump is mostly wrong about China | The China Learning Curve". chinalearningcurve.com . Retrieved 2016-08-03 .

- ^ "XE.com - RUB/USD Chart". world wide web.xe.com . Retrieved 2016-08-03 .

- ^ Moscow, Kathrin Hille- (2014-11-10). "Russia presses ahead with fully floating the rouble". Financial Times. ISSN 0307-1766. Retrieved 2016-08-03 .

- ^ Aleksashenko, Sergey (2014-12-20). "CBR shows how non to intervene". Financial Times. ISSN 0307-1766. Retrieved 2016-08-03 .

- ^ Kitroeff, Natalie (December 16, 2014). "Hither's Why the Russian Ruble Is Collapsing". Bloomberg.

- ^ Tanas, Olga (December 15, 2014). "Russia Defends Ruble With Biggest Rate Ascent Since 1998". Bloomberg.

- ^ Aleksashenko, Sergey (2014-12-20). "CBR shows how not to arbitrate". Fiscal Times. ISSN 0307-1766. Retrieved 2016-08-03 .

- ^ Ostroukh, Andrey; Albanese, Chiara (Dec 3, 2014). "Banking company of Russian federation Spent $700 Million Dec. i Trying to Ease Ruble Pressure". The Wall Street Journal.

- ^ "Russia is burning through its dollar stockpile". Business organization Insider.

- ^ "Bolt: Latest Rough Oil Toll & Chart". NASDAQ.com . Retrieved 2016-08-03 .

- ^ Sachais, Andrew (2015-03-17). "Why The Russian Ruble Is Stabilizing". Retrieved 2016-08-03 .

- ^ Kottasova, Ivana (April x, 2015). "The Russian ruble is upwards twenty% confronting the dollar". CNN.

- ^ Kottasova, Ivana (April 10, 2015). "The Russian ruble is upwardly 20% against the dollar". CNN.

- ^ Ranasinghe, Dhara (2015-04-10). "Russian federation'southward rouble: From down-and-out to darling". CNBC . Retrieved 2016-08-03 .

Source: https://en.wikipedia.org/wiki/Currency_intervention

0 Response to "Companies Can Deal With the Nonconvertibility Problem of Currencies by Engaging in"

Post a Comment